Estimated reading time: 14 minute(s)

Offering their employees affordable health insurance coverage options is important to many employers. One way that they are able to do this is through an Individual Coverage Health Reimbursement Arrangement.

Beginning in the 2020 tax year, employers were given the option to offer this type of coverage to their employees while still meeting their requirements under the Affordable Care Act (ACA). If you are an employer that is interested in offering an ICHRA to your employees, but you just aren’t quite sure where to start, stay tuned because we are sharing all the information that you need to know!

Background Information on the ICHRA

This type of health insurance coverage option is growing in popularity among employers.

An ICHRA, or Individual Coverage Health Reimbursement Arrangement, is an alternative for traditional health insurance group plans. With this type of plan employees choose their own health insurance coverage, potentially from the Healthcare Marketplace. Because their employer receives a tax deduction for these plans, their employees in turn get a tax-free reimbursement.

The employee is initially responsible for the monthly premium and medical expenses related to the plan. Then after submitting the required information to their employer, they will receive set reimbursements.

While this type of plan works for employers of all sizes, this is a great option for small business owners who are seeking to offer their employees some assistance with covering their health insurance expenses each month. This is also a great option for employers who want to offer their part-time employees some assistance with their health insurance expenses.

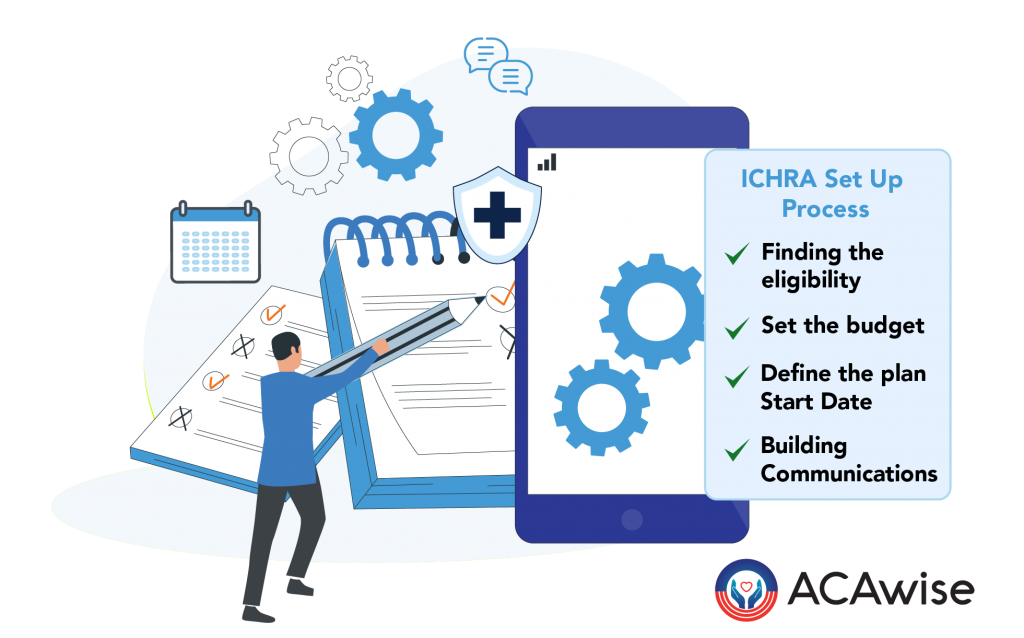

First, decide which employees you’re going to cover

Your first order of business is to decide which employees you are going to include in the ICHRA. Will you offer this new plan to only your full-time employees, or your part-time employees as well? For example, you may decide to cover full-time employees, working at least 30 hours per week, but choose not to offer the ICHRA to part-time employees and seasonal employees. Here are some examples of employee classes:

- Full-time employees

- Part-time employees

- Seasonal employees

- Salaried employees

- Non-salaried employees

- Hourly employees

- Temporary employees working through a staffing company

Next, set the amount you are going to offer

There is no limit to the amount that you can offer to your employees, so it is largely up to you to decide what will work best for you financially.

Remember, you will still need to complete your ACA reporting with the IRS and prove that the plan you are offering is in fact, affordable. So, you will need to do some research to find the amount that your employees will need to ensure that their health insurance is affordable.

The rule that you should follow is this:

Employers should be able to purchase the lowest-cost silver plan available on the local exchange and the expenses from this plan should not exceed 9.78% (for the 2020 tax year) of their gross household income.

Since most employers are unable to find out their employees’ gross household income, they will need to use other methods to calculate the affordability. They can use the Rate of Pay method, or use the Federal Poverty Level method.

Because each of these methods provide an alternative way of calculating the affordability of your ICHRA, they are referred to as Safe Harbors.

This may sound tricky, well, it can be. This is why we decided to create an ICHRA Affordability Calculator, this way we can do the math for you based on the information you provide.

Then, your employees choose their health insurance plan

Once you have determined the amount that you are contributing to your employees on a monthly or annual basis, you will make the offer of coverage to your eligible employees. At this point, it is your employees’ responsibility to find and enroll in a health insurance plan. They have the freedom to choose any plan that fits their needs, however, they must do so within 60 days.

If this offer of coverage happens outside of open enrollment, that’s alright. The ICHRA offer will trigger a special enrollment period for the employee so that they can purchase a plan.

Now, your employees will submit documentation for reimbursement

Your employees will need to submit documentation such as a receipt for medical expenses to you. After approving the request, you will need to reimburse this employee for their expenses up to the maximum amount available to them.

This reimbursement is tax-free money for both you, the employer and your employees. This is another reason that the ICHRA continues to grow in popularity.

Remember, it is very important that your employees don’t apply for Premium Tax Credits in the marketplace, this will not only make them in-eligible for the ICHRA, but you will be penalized by the IRS.

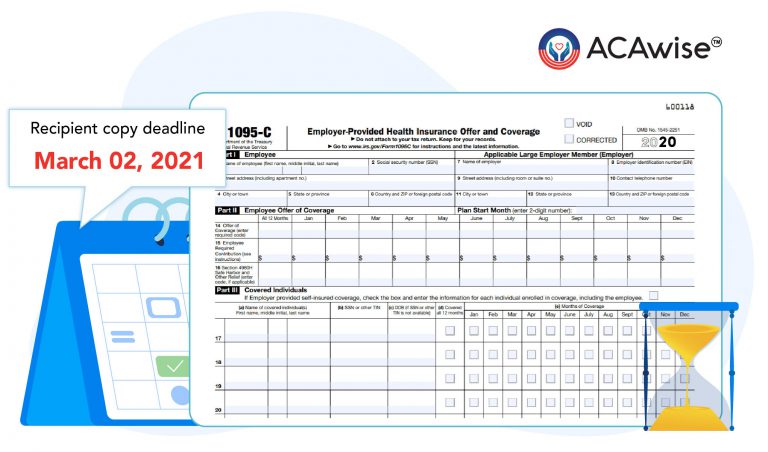

ICHRA reporting requirements

Have you heard about the changes to Form 1095-C for tax year 2020? The IRS has created a new series of codes for employers offering the ICHRA.

Don’t go it alone, call in the experts! Our team at ACAwise can help complete your ACA reporting by generating your forms, codes and all!

Learn more about our services today!

Leave a Comment